Despite growing awareness around financial literacy, India continues to lose an estimated ~US$100 million each year to Ponzi schemes. In many parts of the country, financial education has come too late, only after countless individuals have already fallen victim.

A stark example is Manipur, which, according to a CRISIL report, ranks lowest in financial literacy among smaller Indian states and has the weakest mutual fund penetration in the country. This combination of low awareness and limited access to formal investment options makes for a fertile ground for fraudulent schemes.

What is a Ponzi Scheme?

A Ponzi scheme is a deceptive investment operation that promises high returns with little or no risk. Unlike legitimate investments that generate profits through actual economic activity, Ponzi schemes rely on funds from new investors to pay returns to earlier ones, creating an illusion of profitability. The term originates from Charles Ponzi, who infamously defrauded investors in the 1920’s through a scheme based on the exchange of international postal coupons.

These schemes often appear credible in their early stages, as initial investors receive seemingly impressive returns, encouraging further participation. A recent example is the multi-crore fraudulent investment scheme, which came to light last year after duping thousands of investors which involving a complex network of financial manipulation and money laundering. However, like all such schemes, it unravelled once the inflow of new money dried up, leaving most investors with severe losses. The model is fundamentally unsustainable and collapses once the influx of new investments slows.

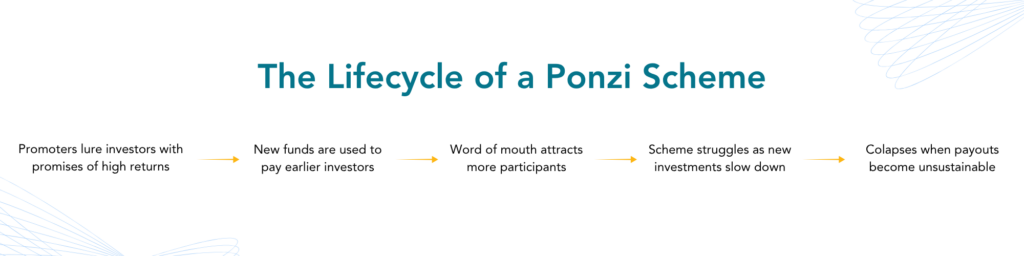

Lifecycle of a Ponzi Scheme

Ponzi schemes typically follow a predictable pattern, beginning with a promoter offering unusually high and consistent returns with minimal risk. Initial investors are paid returns not from legitimate profits, but from the capital contributed by newer participants. This illusion of success helps build credibility and spreads quickly through referrals and perceived trust, attracting a larger number of investors.

The progression of a Ponzi scheme includes:

- Launching the scheme with promises of high returns

- Paying early investors using funds from new participants

- Attracting more investors through perceived success and social referrals

- Facing pressure when recruitment begins to slow

- Failing when incoming funds can no longer meet payment commitments

Common Red Flags

While some Ponzi schemes are elaborate and well-disguised, there are consistent warning signs that investors should watch for:

- Unrealistically high or consistent returns: Guaranteed returns that defy natural market fluctuations are a significant red flag.

- Lack of transparency: Vague explanations about how the investment works or where the returns come from should raise suspicion.

- Pressure to reinvest: Promoters often discourage withdrawals or entice participants to reinvest earnings, delaying the collapse.

- Unregistered investments: If the scheme is not registered with financial regulators like SEBI, that’s a serious warning sign.

- Referral incentives: Aggressive encouragement to recruit others, often with commissions, shifts focus from investment to recruitment.

The Way Forward

Ponzi schemes call for a robust compliance-led strategy underpinned by proactive governance and regulatory vigilance. Financial literacy must be reinforced through structured programs embedded in schools, workplaces, and community outreach to help individuals identify red flags and make informed choices.

Simultaneously, regulatory bodies must enhance compliance mechanisms through tighter monitoring, mandatory disclosure, and stronger enforcement actions to detect and dismantle fraudulent schemes before they escalate.

Never forget that if it sounds too good to be true, it usually is!